Retail therapy: Inside the business shift at L&T Finance

2024-07-21

Transforming L&T Finance: A Fintech-Inspired Makeover

Roy, a seasoned financial professional with over two decades of banking experience, has been entrusted with the task of revolutionizing the non-banking subsidiary of Larsen & Toubro, the renowned engineering giant. His mission is to reshape L&T Finance, making it as nimble and efficient as a fintech player, and carving out a distinct identity for the lender in the financing arena.

Streamlining for Success: L&T Finance's Ambitious Overhaul

Shedding the Wholesale Burden

L&T Finance's past has been marked by a heavy reliance on wholesale loans, funding infrastructure and real estate projects. This concentration on the wholesale segment has been a significant contributor to the lender's lackluster performance over the years, much to the dismay of its parent company. In a bold move, the group has decided to exit the wholesale loans business, a decision that was announced by the then L&T chairman, A.M. Naik, in 2022. Naik acknowledged the underperformance of L&T Finance, stating that the group's own board members had expressed a desire for greater involvement to drive the desired ideas and strategies.The wholesale loans segment had formed a substantial 62% of L&T Finance's portfolio as of March 2016, according to data from Crisil. This concentration was a result of the parent's presence in those segments and the group's overall focus on infrastructure. However, the wholesale business had become a burden, with Naik admitting to "very bad NPAs, particularly in the wholesale and realty businesses." To address this, the group has been actively seeking to sell off these non-performing wholesale loans, even at a loss, in order to concentrate more on the retail segment.

Embracing Retail: A Shift in Focus

As the wholesale business is being phased out, L&T Finance is now entirely focused on retail loans, which currently account for 94% of its total loan book of ₹85,565 crore as of 2023-24. This shift towards retail was initiated under the leadership of former CEO Dinanath Dubhashi, who retired in April 2023 after a 16-year tenure.The group is now banking on Sudipta Roy, a former consumer banking and payments professional from ICICI Bank, to steer L&T Finance towards a high-growth trajectory. Roy, who joined as the Chief Operating Officer in July 2023 and took over as the CEO in January 2024, has been given a free hand to streamline the business and focus on performance delivery in terms of credit cost and top-line growth.

A Five-Pillar Strategy for Transformation

To propel L&T Finance's growth, the management has devised a comprehensive five-pillar strategy, which was announced in October 2023. These five pillars are:1. Raising brand visibility: Roy recognized that while the L&T brand is well-known and respected in urban India, L&T Finance was perceived to be predominantly a rural-focused lender. He aims to enhance the company's brand presence and association in urban areas.2. Enhancing customer acquisition: The NBFC is focused on expanding its customer base, particularly in the high-velocity credit businesses where quick decision-making is crucial.3. Sharpening credit underwriting: The introduction of "Project Cyclops," a credit risk assessment and automated decision-making digital credit engine, leverages Artificial Intelligence (AI) and Machine Learning (ML) to enhance the company's underwriting capabilities.4. Building a futuristic digital architecture: L&T Finance is investing in technology to streamline its operations and improve efficiency, with the goal of becoming a more agile and nimble player in the market.5. Building capabilities: The company is focused on developing the necessary skills and expertise within its workforce to support its transformation and growth aspirations.

Technological Advancements: Powering the Transformation

One of the key initiatives driving L&T Finance's transformation is the implementation of "Project Cyclops," a credit risk assessment and automated decision-making digital credit engine. Developed internally by a team of 100 developers at a cost of around ₹5 crore, this three-dimensional credit engine utilizes AI and ML to assess the repayment capability and credit quality of potential customers.The primary objective of Project Cyclops is to enable quick and accurate decisions, particularly in high-velocity credit businesses such as two-wheeler financing, where a delay in decision-making can lead to customers seeking alternatives. The system is currently being used in 25 two-wheeler dealerships and is expected to be scaled up to 100% of the two-wheeler loan portfolio within the next 45 days. After the two-wheeler segment, the credit engine will be deployed in tractor financing, small business loans, and eventually, mortgages and personal loans.Roy believes that Project Cyclops will significantly improve the company's underwriting standards and decision-making processes, ultimately enhancing the overall quality of its loan portfolio.

Early Signs of Progress

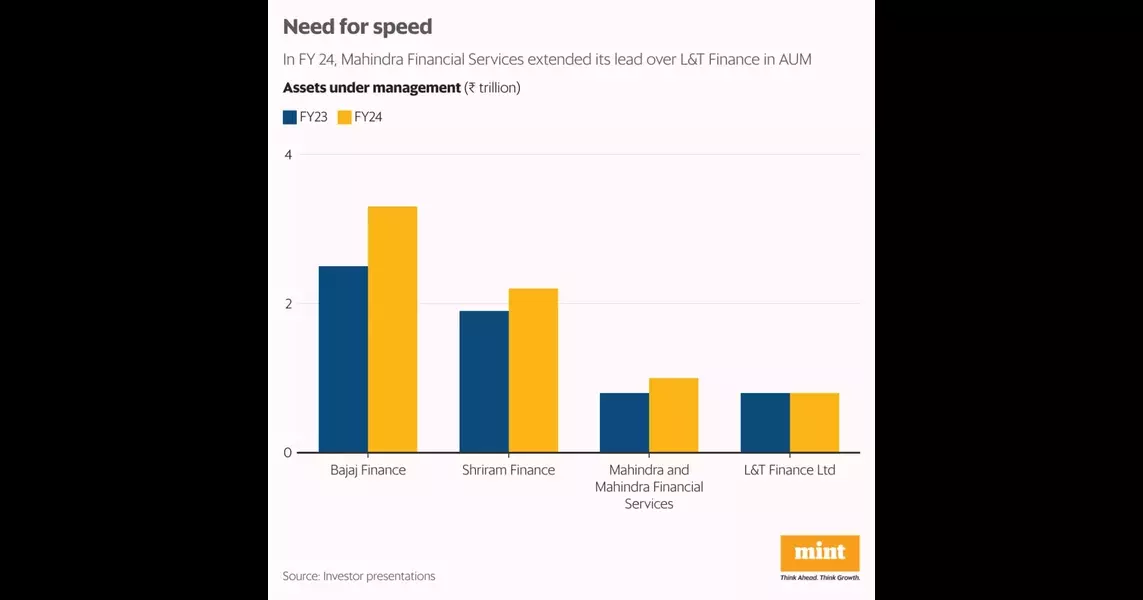

While it is still early to assess the full impact of the changes implemented at L&T Finance, there are already visible signs of progress. The company has reported a notable increase in its two-wheeler loan disbursements, which have grown from ₹550-600 crore per month a year ago to ₹900-1,000 crore per month currently. Additionally, the share of prime (better-rated) customers in two-wheeler loan disbursements has increased from 37% in the June quarter of the previous year to 50% by the end of 2023-24.In the aggregate mortgages and loans against property segment, L&T Finance's monthly disbursements have also increased from ₹550-600 crore to close to ₹900 crore. Similarly, in the rural business finance segment, the company has seen a rise from ₹1,550-1,600 crore per month to ₹1,900-2,000 crore per month.Roy has set an ambitious goal of growing the company's retail loan book to ₹2 trillion by 2027-28, which would place it on par with the loan books of Federal Bank and Yes Bank.

Navigating Regulatory Challenges

While L&T Finance is focused on its growth trajectory, it must also navigate a stricter regulatory environment. In September 2022, the Reserve Bank of India (RBI) classified the NBFC as an "upper-layer" entity, subjecting it to enhanced regulatory requirements for at least five years.This classification posed a challenge, as the RBI regulations mandated upper-layer NBFCs to go public within three years of being identified as such. To address this, L&T Finance underwent an internal restructuring, merging L&T Finance, L&T Infra Credit, and L&T Mutual Fund Trustee into the listed L&T Finance Holdings Ltd (LTFH), effectively avoiding the need for a separate listing of L&T Finance.Roy believes that the harmonization of regulations between banks and upper-layer NBFCs has been beneficial, as it allows L&T Finance to consider itself on par with banks and adhere to the same regulatory standards.However, the NBFC sector as a whole is facing a slowdown in growth, partly due to the RBI's decision to increase the level of capital that banks need to set aside for retail loans and loans to NBFCs, raising risk weights by 25 percentage points to 125%. This move is aimed at curbing the growth of the sector and lowering systemic risk.Despite these challenges, Roy remains optimistic about L&T Finance's ability to deliver results. He emphasizes the company's agility and nimbleness as a non-banking financial services provider, which he believes will enable it to navigate the evolving landscape more effectively than traditional banks.